November 2021 – Black Friday All Month

Portfolio Manager comment Coeli Frontier Markets Fixed Income November 2021

Summary

The Fund lost 4.63% gross of fee in November as the market lost any demand for risky frontier or emerging market debt. Spread to US treasuries increased to 841bp, the highest in 12 months. Main losses came from positions in El Salvador, Sri Lanka and Ghana.

Weakness in our market was initially driven by continued fear of (i) rising inflation globally and (ii) rising US treasury yields. Then came negative covid-19 headlines regarding vaccine efficacy, a new mutation and lock downs in Europe.

Key Market Developments

At the end of the month covid once more took the centre stage. The main vaccines are shown to be less effective in preventing infection and deteriorate over time. A new coronavirus mutation was discovered in South Africa which appears to spread faster. And not least, European countries have started to introduce full or partial lockdowns.

The “risk off” sentiment didn’t just affect the frontier market but our market was very fast to price in a probability of a March 2020 scenario. This also included a correction in the commodity space with significant drops in oil prices.

The second major event of the month was the hawkish re- appointment of Jerome Powell, followed by the Federal Reserve acknowledging inflation and accelerating the taper of quantitative easing (“QE”).

Frontier debt was an underperformer in November compared to other credit asset classes. The downside of being among the most liquid high yield rated asset classes is that it is also the one often used to manage overall risk in emerging market portfolios. The flipside of the coin is that we are also fast to recover.

In the frontier space, the military situation in Ethiopia continued to deteriorate in November with bonds dropping over 17%. In the wider EM universe, Turkey has been in the headlines with the collapse of their currency by 28% over the past month on the back of the president’s policies.

Portfolio Developments

Ghana, our largest position, continued to trade poorly as the budget proposal for next year wasn’t taken well by the market, in part due to a larger deficit of 12%. This is on the back of more conservative accounting for legacy costs due to support for the financial and utility sector. The budget deficit is expected to narrow towards 8% in 2022 as authorities expect a sharp increase in revenues, partly on the basis of a financial e-transaction tax.

Sri Lanka was also a poor performer losing over 9% in November. The market is waiting for authorities to come up with a credible plan to solve the foreign reserve shortage. An agreement with the IMF could be it but doesn’t seem likely. Despite the volatility in the short term, we continue to view Sri Lanka bonds attractive also in the event of a restructuring of the bonds.

El Salvador bonds were the third large underperformer in November. Animosity with the US and more bitcoin headlines, including a “bitcoin bond” was not well received. At the same time the IMF finalised their Article IV report on El Salvador, and it wasn’t all bad news as they were impressed by the strong recovery after covid and the handling of the covid situation in general. The IMF’s biggest concern was, again, bitcoin. But the statement also lacked any details on any immediate funding. We find the statement supportive for achieving a needed program during 2022.

Top 3 and Bottom 3 Contributors in Q3

TOP |

BOTTOM |

| Honduras – Post election recovery | El Salvador – Animosity with the US & bitcoin |

| Kazakstan – Matured bond | Sri Lanka – Continued shortage of hard currency reserves |

| Uzbekistan – Stable local currency performance | Ghana – Deficit update and disappointing 2022 budgetSource: Coeli; Bloomberg; Based on Q3 2021 contribution to the fund’s performance |

Source: Coeli; Bloomberg; Based on November 2021 contribution to the fund’s performance

During the month we made a number of changes to the portfolio. Firstly, we have continued to build up our position in Egypt which was 4.4% at month end. Egypt has been among the most favoured high yield rated bonds but has suffered as a crowded long during the risk-off period. Secondly, we have closed out of our exposures in Vietnam and Pakistan, in both cases on the back of strong relative performance and tight pricing. Further, we reduced our position in the defensive position in Namibia by 2.8% and rebalanced our higher risk positions.

Outlook

We ended the month with a total risk level of 118% and a yield of 9.6%. Cash balance was unusually high due to FX moves at month end. Despite the risk level being slightly lower, we estimate our market beta to have increased over the month on the back of our growing position in Egypt.

It’s too early to draw conclusions about the consequences of the new covid variant, but it will add to volatility until a consensus view is established. The acknowledgement of inflation and the accelerated taper of QE in the USA makes it for a difficult outlook for emerging markets.

Frontier markets have already taken a significant beating and repriced with the fund yield at 9.6%. Equally our fund is exposed to numerous idiosyncratic situations which we expect to outperform the wider EM debt space over the next year.

Finally we have some positive supernational events ahead. In addition to the IMF’s delayed SDR re-allocation, the EU has just published more details on its initiative, Global Gateway, to support developing countries.

EU’s Global Gateway investment launch facts |

|

| What: Infrastructure investments across digital, climate and energy, transport, health, education and research | |

| Amount: Up to €300bn of investments between 2021 and 2027 | |

| Who: EU’s Delegations globally will be key to indentify and coordinate projectsWith a yield of 8.6%, spread of 741 bps, and substantial exposure to commodity exporting countries we believe the fund is well positioned to weather continued interest rate uncertainty but also benefit from a return of risk appetite in the wider EM space. |

Source: EU

The fund continues to benefit from coupon payments in excess of 0.5% per month from its holdings.

Kind Regards, Lars and Maciej

| Fund metrics 1) | Fund | NEXGEM 2) |

| Total fund assets (USDm) | 39 | |

| Yield to worst (%) | 9.6 | 8.3 |

| Spread (bps) | 841 | 711 |

| Running yield (%) | 6.0 | 6.3 |

| Spread duration (years) | 5.3 | 5.7 |

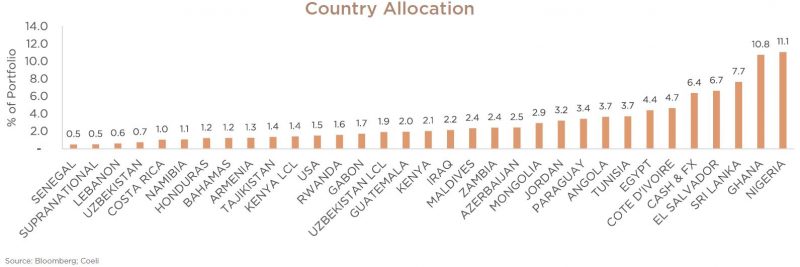

| Number of countries | 30 | 36 |

| Number of bonds | 72 | 151 |

| Performance | MTD | QTD | Since launch |

| Fund (before fees) | -4.63% | -5.26% | -2.33% |

| Fund (I USD) | -4.71% | -5.41% | -2.97% |

| Benchmark (NEXGEM) | -4.28% | -4.48% | -1.75% |

DISCLAIMER. This is a marketing communication.

Before making any final investment decisions, please refer to the prospectus of Coeli SICAV I, its Annual Report, and the KIID of the relevant Sub-Fund. Relevant information documents are available in English at coeli.com. A summary of investor rights will be available at https://coeli.customer01.tgen.se/regulatory-information-coeli-asset-management-ab/.

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

Neither past performance nor simulated performance is an indicator or a guarantee of future performance Estimates of future returns should not be construed as a guarantee of future performance The value of bonds in the Fund and income received from it can go down as well as up, and investors may not get back the full amount invested. This material is not intended to be distributed in the USA or other countries where the content or the distribution may be prohibited The fund described herein may not be offered or sold to US citizens or residents of the USA or to a corporate, partnership or other entity created or organized in or under the law of the USA Although the information has been based on sources deemed be reliable, Coeli cannot guarantee its accuracy and assumes no liability whatsoever for incorrect or missing information nor for any loss, damage or claim arising from the use of the information in this material.